Window Replacement Financing Options Explained: A Comprehensive Guide

Explore various financing methods for your window upgrade project.

Do you dream of new windows but worry about the upfront cost? Many homeowners delay window replacement due to money issues.

What if you could upgrade your windows now and pay later? Understanding your financing choices can make that happen.

This guide covers window replacement financing options. It helps you make smart choices and improve your home.

Replacing your windows is a big investment. It can change your home's look, energy use, and value. But, the starting cost can be a problem. Many financing options are available. They help you spread out the cost. This guide looks at different financing methods. It includes loans, credit, and plans from window companies. The goal is to give you the information you need. Then, you can pick the best financing for your needs. You can enjoy new windows sooner. For more information, read about window replacement costs here.

Quick navigation

What this means for you

Choosing the right financing lets you upgrade your home. You do not have to use your savings or take on too much debt. It allows you to improve your home's energy use, comfort, and look. You can have lower energy bills, a quieter home, and a better look sooner. Also, your home's value will go up if you sell. By knowing about financing, you can make good choices. This makes window replacement easier. It can also help you figure out the total window replacement cost. You can find this here.

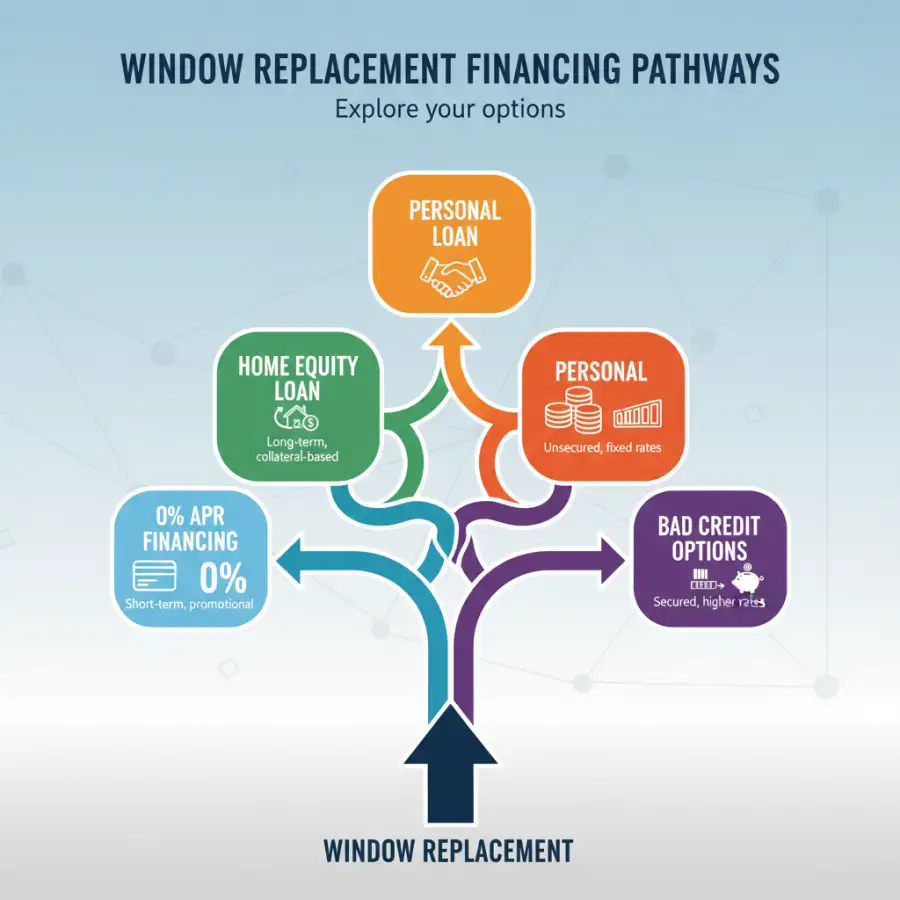

Types of Financing Options for Window Replacement

Several financing options exist for window replacement. Each has its own good and bad points. Knowing these options helps you make a choice based on your money situation. Let's look at the most common types of financing:

Home Equity Loans and Lines of Credit (HELOCs): These use your home's value as collateral. A home equity loan gives you a lump sum. A HELOC offers a line of credit. Interest rates can be good. The interest may be tax-deductible. But, you could lose your home if you do not pay back the loan. It is a risk, but it can give you the best terms.

Personal Loans: Personal loans are not secured. This means they do not need collateral. They often have fixed interest rates and payment schedules. Personal loans are usually easier to get than home equity loans. But, interest rates may be higher. They are useful if you do not want to risk your home. Always compare rates and terms from different lenders.

Credit Cards: Using a credit card can be easy, especially if the card has a 0% introductory APR. But, high-interest rates can happen quickly if you do not pay the balance. Think about the interest rates and fees. Also, be sure you can pay off the debt fast. This can be a good short-term solution.

Manufacturer-Specific Financing: Many window companies offer financing. These plans may have special deals, like 0% financing for a certain time. The terms and conditions vary. Compare different offers before you commit. This can often be the easiest option.

Government and Utility Programs: Some government programs and local utilities offer rebates, grants, or low-interest loans. They are for energy-efficient home improvements, like window replacement. Research these options in your area. They can lower your costs.

Understanding Interest Rates and Terms

It is important to understand interest rates and loan terms. The interest rate decides how much you pay to borrow money. The terms explain the payment schedule. Here is a breakdown of what to consider:

Interest Rates: Interest rates can be fixed or variable. Fixed rates stay the same during the loan. This provides certainty. Variable rates change with the market. This can be good when rates are falling. But, your payments can go up if rates rise. It is important to compare interest rates from different lenders. Then, you can find the best terms.

Loan Terms: Loan terms (the payment period) can be from a few months to several years. Longer terms usually mean lower monthly payments. But, they cost more in interest. Shorter terms mean higher payments. But, you pay less total interest. Pick a term that balances cost and affordability.

APR (Annual Percentage Rate): The APR includes the interest rate and other fees. This gives you a better view of the total cost of borrowing. Always compare APRs when looking at financing.

0% Financing: Some manufacturers and credit cards offer 0% introductory APR periods. This can be a good option. But, be sure you can pay back the balance before the deal ends. This avoids high-interest charges.

Eligibility Criteria and Credit Scores

Lenders use credit scores and other things to check your creditworthiness. A higher credit score often means better interest rates and terms. Understanding the requirements can help you. It can also improve your chances of approval:

Credit Score: Your credit score is a key factor. It decides your eligibility and interest rate. Check your credit score from all three credit bureaus before you apply. You can get a free credit report from each bureau every 12 months.

Income and Employment: Lenders will check your income and job history. They want to be sure you can pay back the loan. Be ready to give them pay stubs, tax returns, and job verification.

Debt-to-Income Ratio (DTI): Your DTI compares your monthly debt payments to your monthly income. A lower DTI shows less risk. Lenders often want a DTI below 43%. Figure out your DTI to see where you stand.

Collateral (for secured loans): If you apply for a home equity loan or HELOC, the lender uses your home as collateral. If you do not pay back the loan, you could lose your home. Be sure you know the risks before you start.

Tax Benefits and Incentives

You may get tax benefits and incentives, depending on where you live and the financing type. These can lower the overall cost of your window replacement.

Energy Efficiency Tax Credits: The US government and some states offer tax credits. These are for energy-efficient home improvements. See if your new windows qualify. The IRS has specific rules. You must meet them to get the credits. It is a good idea to talk to a tax professional.

Rebates and Grants: Utility companies and local governments often give rebates or grants. These are for energy-efficient upgrades. Research programs in your area. They can save you money. These incentives can make window replacement more affordable and better for the environment.

Interest Deductibility: In some cases, you can deduct interest paid on home equity loans. Talk to a tax advisor. See if you can deduct the interest payments. Always talk to a tax professional for help with tax benefits.

Financing Options from Major Window Companies

Many window companies offer financing. This can make the process easier. Knowing about the programs of some top companies will help you make a good choice.

Renewal by Andersen: Renewal by Andersen offers different financing options. These include 0% interest for a limited time. Their programs often have flexible terms. They fit different budgets. Check the details of their offers. They often run special deals. It pays to be informed.

Pella: Pella offers financing through partnerships with financial institutions. Their plans may have fixed rates, flexible terms, and deals. What is available depends on where you live and the current deals. Check what is available now. Look closely at their financing options.

Other Companies: Many other window companies, like Champion Windows, offer financing. Look at these options. Compare terms, rates, and deals. Researching multiple companies can help you find the best financing. Always read the fine print before you commit.

Risks, trade-offs, and blind spots

Financing can make window replacement easier. But, it is important to think about the risks, trade-offs, and things to watch out for.

High-Interest Rates: If you have a low credit score, or choose high-interest financing, the total cost of your window replacement will go up. Always compare rates and terms.

Debt Burden: Taking on debt can strain your budget. Be sure you can afford the monthly payments. Think about how it affects your money.

Hidden Fees: Some financing plans have hidden fees. These include origination fees, penalties, or late fees. Carefully read all terms before you sign. This ensures you know all the costs.

Overspending: Financing can make it easier to spend more. Set a budget. Stick to it. Avoid spending too much. Get multiple quotes. This makes sure you get the best deal on the windows.

Main points

- Explore financing options. These include home equity loans, personal loans, and credit cards.

- Understand interest rates, loan terms, and APRs. Then, you can make informed choices.

- Check your credit score. Meet the requirements before you apply.

- Look at tax benefits, like energy efficiency tax credits and rebates.

- Compare financing options from window companies like Renewal by Andersen and Pella.

- Think about the risks, like high-interest rates and debt.

- Set a budget and stick to it. This avoids overspending.

- Review all terms before you sign any agreement.

Financing can help you manage and afford window replacement. Research your options, compare terms, and understand the risks. You can choose the right financing. Then, you can enjoy new windows in your home. Are you ready to start? Consider the total window replacement cost here.